Business

European Markets Decline Amid Geopolitical Tensions and Fed Decision Anticipation

European stock markets opened lower on Wednesday, impacted by escalating geopolitical tensions in the Middle East and uncertainty surrounding U.S. trade policies. Healthcare and technology stocks led the declines, with major indices slipping in early trading.

European Market Performance

The FTSE 100 in the UK dropped 0.3%, weighed down by losses in companies such as Compass Group plc, GSK plc, and Flutter Entertainment. Germany’s DAX index also declined by 0.3%, with Siemens AG and Deutsche Bank AG among the biggest losers. Meanwhile, France’s CAC 40 slipped 0.2%, and the broader STOXX 600 index fell by 0.3%.

Investor sentiment remained cautious amid rising tensions in the Middle East, where Israel launched its most intense airstrike on Gaza since a ceasefire agreement with Hamas in mid-January. Additionally, Russian President Vladimir Putin ruled out a ceasefire with Ukraine, maintaining his stance on continued attacks against Ukrainian energy infrastructure.

Adding to market concerns, former U.S. President Donald Trump reiterated that sectoral and reciprocal tariffs would come into effect on April 2. Investors are also closely monitoring the U.S. Federal Reserve’s interest rate decision, expected later on Wednesday.

Kyle Chapman, an FX markets analyst at Ballinger Group, noted that while geopolitical and trade policy concerns persist, markets are temporarily shifting focus to a series of central bank decisions expected in the coming days. “I suspect [Federal Reserve Chair Jerome] Powell would prefer to skip today’s rate decision given the impossible job of creating economic projections in this environment,” he said.

Asia-Pacific Market Overview

In Asia, markets exhibited mixed performances. Japan’s Nikkei 225 fell by 0.3% to 37,751.9 after the Bank of Japan kept interest rates unchanged, as expected. Analysts at Pantheon Macroeconomics noted that the BoJ’s caution stemmed from uncertainty over potential U.S. tariffs under the Trump administration.

China’s Shanghai Composite Index dipped 0.1% to 3,426.4 as markets pulled back from recent gains fueled by optimism over the tech sector and stimulus measures. Growing concerns over U.S. restrictions on Chinese access to semiconductor technology also contributed to the decline. Meanwhile, Hong Kong’s Hang Seng Index inched up 0.1% to 24,771.1.

Australia’s S&P/ASX 200 index closed 0.4% lower at 7,828.3, while South Korea’s Kospi index bucked the trend, rising 0.6% to 2,628.6.

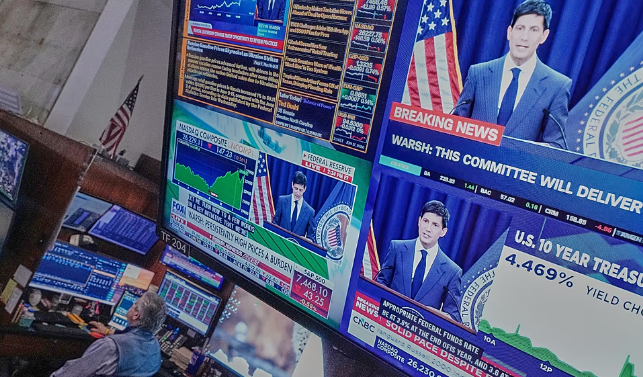

U.S. Market Performance

Wall Street closed lower on Tuesday, retreating from a two-day rally as investors awaited the Federal Reserve’s rate decision. The S&P 500 declined by 1.1%, dragged down by losses in cruise companies such as Royal Caribbean Cruises and Norwegian Cruise Line, along with a dip in Tesla’s stock. The NASDAQ 100 tumbled 1.7%, with significant losses in AppLovin, Tesla, and Mercado Libre, though Intel and Coca-Cola European saw gains. Meanwhile, the Dow Jones Industrial Average dropped 0.6%, with Nvidia and IBM among the biggest decliners.

Commodities and Currency Movements

In the commodities market, U.S. crude oil prices slipped 0.4% to $66.6 per barrel, while Brent crude oil also fell by 0.4% to $70.3 per barrel. Gold hit a fresh record high, rising 0.3% to $3,040.8 per ounce, as investors sought safe-haven assets amid geopolitical uncertainties.

In the forex market, the euro weakened against the U.S. dollar, with the EUR/USD pair dropping 0.4%. However, the EUR/GBP pair advanced by 0.2%, reflecting continued volatility in currency markets.

As global markets navigate a volatile environment, investors are closely watching upcoming central bank decisions and geopolitical developments for further direction.

Turkey has emerged as the most affordable holiday destination among seven of Europe’s most popular tourist countries, while Portugal offers the best value for hotels and restaurants, according to a Euronews Business analysis of Eurostat price data.

The comparison examined national average prices across Turkey, Portugal, Spain, Greece, Croatia, Italy and France, covering a wide range of consumer goods and services. Although prices in major tourist resorts can vary from national averages, the data provides a broad picture of what travellers can expect when planning summer holidays.

Using Eurostat’s Household Final Consumption Expenditure price index, which measures the average cost of more than 2,000 goods and services, Turkey ranked as the least expensive destination overall. A basket of goods and services costing €100 across the European Union would cost about €59.60 in Turkey, making it roughly 40% cheaper than the EU average.

France was the most expensive country in the survey, with average prices slightly above the EU benchmark at €100.30. Italy followed at €97.10, while Spain, Greece, Portugal and Croatia all recorded lower overall price levels than the European average.

Accommodation and dining costs showed even greater differences. Portugal offered the lowest prices for hotels and restaurants, with a price index of 73.6, meaning visitors could expect to pay more than 26% less than the EU average for meals and lodging. Turkey ranked second in this category with a score of 78.3, while Spain and Greece also remained below the European average.

France proved to be the most expensive destination for accommodation and restaurant services, followed by Italy.

Food prices varied less dramatically across the countries. France again recorded the highest average grocery costs, with food prices almost 8% above the EU average. Turkey remained the least expensive for food shopping, while Spain was the only other country where food prices were below the European benchmark.

One category where Turkey stood out for a different reason was alcohol. Despite being the cheapest destination overall, alcoholic beverages were by far the most expensive among the countries surveyed. Alcohol prices were more than double the EU average, largely reflecting the country’s high taxes on alcoholic drinks.

Italy offered the lowest alcohol prices, while Spain also remained below the European average. Greece and Croatia recorded relatively high prices for alcoholic beverages.

Turkey also had the lowest tobacco prices by a considerable margin and ranked as the cheapest destination for public transport. France was the only country where public transport costs exceeded the EU average.

Seafood prices were comparatively stable across all seven destinations, with only modest differences between countries.

The analysis noted that the figures reflect national averages rather than prices in individual holiday resorts. It also does not account for differences in income levels, meaning affordability may vary depending on where travellers are visiting from.

The European Union has moved a step closer to introducing the digital euro after the European Parliament approved its negotiating position, clearing the way for final discussions with member states on the proposed digital currency.

The vote in Strasbourg marks the beginning of the last phase of negotiations between the European Parliament and EU governments. Lawmakers and national representatives are expected to focus on several complex issues, including how banks and payment providers will be compensated for offering digital euro services and how transaction fees will be distributed across the payment system.

The digital euro is planned as an electronic version of central bank money issued and guaranteed by the European Central Bank (ECB). Officials have repeatedly stressed that the new currency is intended to complement physical cash rather than replace it, while also working alongside existing banking and payment services.

Under the proposal, consumers would be able to store digital euros in a dedicated electronic wallet. A maximum holding limit will be introduced, although the exact amount has not yet been decided.

The system is expected to support both online and offline payments, allowing transactions even when internet access is unavailable. Privacy has also been presented as a key feature of the project. According to the proposal, the ECB will operate the underlying infrastructure but will not be able to directly identify users through their payment data.

Commercial banks and payment service providers will be responsible for offering digital euro accounts and related services to individuals and businesses, creating a partnership between the central bank and the private financial sector.

According to sources familiar with the negotiations, the most challenging issue remains the compensation model. Negotiators must determine which financial institutions will receive payments for providing digital euro services, how much compensation they should receive and how those payments will be financed.

Another important topic is the distribution of transaction fees throughout the payment chain. Current proposals suggest merchants would pay lower fees than those typically charged for traditional card payments, a move that supporters believe could reduce business costs and encourage wider adoption of digital payments.

The negotiations are expected to intensify during the autumn as lawmakers seek to resolve outstanding disagreements before presenting the final legislation.

If agreement is reached, EU institutions aim to grant final approval before the end of the year. The European Central Bank is expected to begin a pilot programme in 2027 to test the system before a wider public rollout.

Current plans envisage the digital euro becoming available for everyday retail payments in 2029. European officials view the initiative as an important step toward strengthening the region’s payment infrastructure, improving financial resilience and providing consumers with a secure public digital payment option in an increasingly cashless economy.

The outlook for the global economy during the remainder of the year will depend largely on whether the fragile peace agreement between the United States and Iran survives, according to a new analysis by Oxford Economics, which says the deal could determine the direction of inflation, energy prices and financial markets.

After a first half marked by conflict in the Middle East, volatile oil prices and rapid growth in artificial intelligence investments, the consultancy believes the next six months will be influenced by a series of interconnected risks, with the US-Iran truce standing at the center.

Chief Global Economist Ryan Sweet said the durability of the agreement would determine whether the global economy benefits from lower energy costs or faces another oil-price shock.

Oxford Economics forecasts global annualized economic growth of 3.1 percent during the second half of the year, compared with an estimated 1.6 percent in the first six months. The projection assumes oil prices remain relatively stable, supporting consumer spending and easing inflationary pressures. However, Sweet described the chances of the peace agreement holding as no better than “a coin flip.”

The report expects Brent crude to average in the low $70s per barrel if the agreement remains intact. A breakdown, however, could trigger higher inflation, tighter financial conditions and renewed pressure on global supply chains.

Those concerns intensified after fresh military exchanges on Wednesday. The United States launched strikes against Iran following allegations that Tehran had attacked three commercial vessels in the Strait of Hormuz. Iran responded with strikes targeting Bahrain and Kuwait, raising fears that the ceasefire could unravel.

Oil markets reacted quickly, with Brent crude climbing above $78 a barrel after rising more than six percent during trading.

Oxford Economics said any disruption would extend well beyond energy markets. Higher oil prices could increase production costs for technology companies, disrupt semiconductor supply chains across Asia, complicate central bank policy decisions and influence political developments, including upcoming elections in the United States and Israel.

The consultancy’s outlook differs from several other major forecasts. Morgan Stanley expects crude prices to approach $90 a barrel by year-end, while the World Bank projects Brent crude to average around $94 this year and anticipates global economic growth slowing to 2.5 percent in 2026.

Oxford Economics identified shipping activity through the Strait of Hormuz as one of the clearest indicators of whether the peace agreement is holding. The report said a sustained recovery in vessel traffic by mid-July would strengthen confidence in the deal.

Beyond geopolitics, the report highlighted growing risks surrounding the artificial intelligence sector. The Bank for International Settlements recently warned that rapid expansion in AI investment has become increasingly dependent on private credit and complex financing arrangements outside the traditional banking system.

Oxford Economics also modeled a scenario in which US technology stocks fall by 25 percent over one year. According to Sweet, such a correction would bring US economic growth close to a standstill and reduce global growth by more than one percentage point.

Despite these risks, the consultancy said stronger AI-driven productivity and resilient economic activity in Europe could provide support if geopolitical tensions ease and energy markets stabilize during the second half of the year.

Police Launch Major Operation After Woman Taken Hostage in Berlin Supermarket

Late Merino Strike Sends Spain Into World Cup Semifinals Against France

Turkey Offers Cheapest Holiday Costs in Europe, While Portugal Leads for Hotels and Dining

European Authorities Dismantle International Tobacco Smuggling Networks, Seize Millions of Illegal Cigarettes

EU Plans Tougher Public Procurement Rules to Limit Security Risks From Foreign Firms

EU Advances Digital Euro Talks as Lawmakers Enter Final Negotiation Stage

Oxford Economics Warns US-Iran Peace Deal Will Shape Global Economy in Second Half of Year

Uzbekistan Accelerates Multi-Billion-Dollar Drive to Boost Value-Added Exports

New Blood Test Shows Promise for Earlier Endometriosis Diagnosis

European Parliament Set for Fresh Vote on Controversial ‘Chat Control’ Proposal

Meta Acquires Tilda Swinton VR Doc ‘Impulse: Playing With Reality’

China’s Historic Olympic Victory Sparks National Pride Amid Controversy

Saudi Arabia’s Model for Sustainable Aviation Practices

Recent Developments in Small Business Taxes

Effective Drain Cleaning: A Key to a Healthy Plumbing System

Who was Ebrahim Raisi and his status in Iranian Politics?

Keely Hodgkinson Wins Britain’s First Athletics Gold at Paris Olympics in 800m

Carrectly: Revolutionizing Car Care in Chicago

Nobel Laureate Muhammad Yunus Proposed as Head of Bangladesh’s Interim Government Following Hasina’s Resignation

Chinese Hackers Infiltrate Major U.S. Telecom Firms in Possible National Security Breach

Sony WF-10XM4: Headphones Are Our Absolute Favorite

10 Places You Can’t Miss If It’s Your First Time in European

New Census Data Will Shake Up Alabama Politics

16 Top of Our Favorite Outdoor Clothing Brands

Fashionable Summer Accessories to Dress Up Your Travel Look

How Sleeping Less than 7 Hours a Night Can Lead to Weight Gain

-

Entertainment2 years ago

Entertainment2 years agoMeta Acquires Tilda Swinton VR Doc ‘Impulse: Playing With Reality’

-

Sports2 years ago

Sports2 years agoChina’s Historic Olympic Victory Sparks National Pride Amid Controversy

-

Business2 years ago

Business2 years agoSaudi Arabia’s Model for Sustainable Aviation Practices

-

Business2 years ago

Business2 years agoRecent Developments in Small Business Taxes

-

Home Improvement2 years ago

Home Improvement2 years agoEffective Drain Cleaning: A Key to a Healthy Plumbing System

-

Politics2 years ago

Politics2 years agoWho was Ebrahim Raisi and his status in Iranian Politics?

-

Sports2 years ago

Sports2 years agoKeely Hodgkinson Wins Britain’s First Athletics Gold at Paris Olympics in 800m

-

Business2 years ago

Business2 years agoCarrectly: Revolutionizing Car Care in Chicago